22/03/2019

This is a tale of the Old World of Internal Combustion Engines versus the New of Electrified Powertrains, and of the Giant automotive OEMs versus the Minnows that are automotive start-ups – but mainly statistics showing patent filing trends in the automotive powertrain sector.

Before we begin though, some calibration …

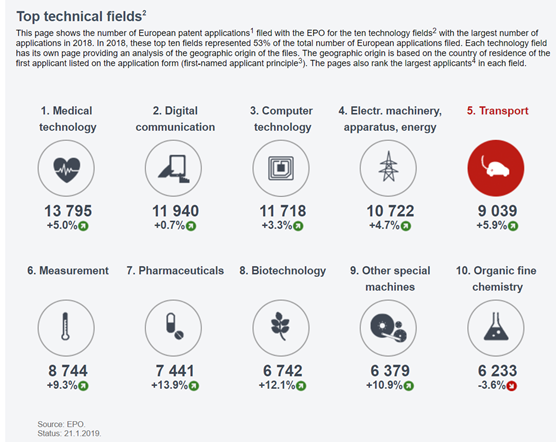

The European Patent Office publishes an annual report showing filing statistics and trends. In 2018, nearly 175,000 European patent applications were filed, about 9,000 of which were in the “Transport” technical field (see an extract below from the EPO’s 2018 annual report). However, this is likely not the full picture of patent filings in the automotive sector, given other technology fields, such as “Electrical machinery, apparatus, energy” and “Other special machines”, will no doubt include patent filings to automotive related technology. Given this, it seems that somewhere between 5% and 10% of patent filings in Europe, and by proxy the world, are likely related to the automotive sector.

Figure 1. [EPO Annual Report 2018]

Calibration over, and so on with our tale which would not be complete without some myths and legends…

MYTH 1: Internal Combustion Engines are a thing of the past

MYTH 2: Chinese companies are not innovators

LEGEND: Toyota are a patent filing powerhouse

We will look at each myth and legend, and come to some understanding of whether they are based on facts. Those “facts” are the results of our searches for patent filings in Europe, the US, Japan, China, and also International (PCT) patent filings, as a proxy for worldwide patent filings, in various patent classifications related to automotive powertrain technology. We eliminated duplicates, i.e. a patent filed to an invention in the US and Europe would only be counted once, so that the numbers should be an approximation of the number of inventions.

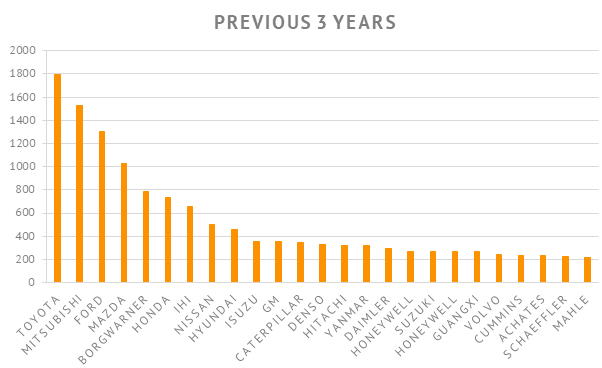

Let’s look firstly at patent filings over the past three years, broken down by applicant, in the patent classification IPC F02B – “Internal Combustion Piston Engines”.

Figure 2.

Figure 2.

As you can see from Figure 2, none of the applicant names come as any real surprise with most of the Giants (i.e. the major OEMs, and Tier 1 companies) making an appearance. We also see the first evidence to back up our “legend” that Toyota are a patent filing powerhouse. At first blush then, the Old World of internal combustion engines is not a thing of the past after all, and the Giants are winning this particular battle. What we can take from these results is that there is likely a significant amount of R&D in this area, but we should consider how the filings are changing over time.

Before doing so though, the more astute amongst you will see that we are equating numbers of patent filings with R&D spend; this is clearly not an ideal analogy, because there other many other factors that will influence the number of patent filings per $ of R&D spend. Nevertheless, it is clear that in order to file a patent application, a certain amount of R&D must have taken place. What our results will not show is where a company has carried out R&D but for some reason decided not to file patent applications to every resulting innovation.

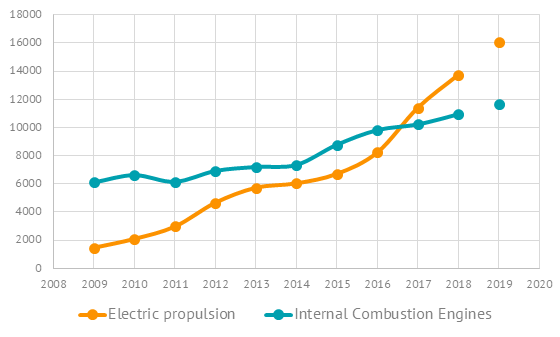

So, let’s now look at how the filings are changing over time. Figure 3. below shows the same patent classification, IPC F02B, but this time shows how the total number of patent filings have changed over the past 10 years. What we see is that the number of filings has been steadily increasing, and our predictions for 2019 (based on the first couple of months of the year) show that the increase is set to continue. That initial finding then, taken from Figure 2., seems correct; the Old World is not yet a thing of the past.

Figure 3.

Figure 3.

What we have also shown in Figure 3. is the number of filings in the New World of electrified powertrains, patent classification IPC B60L 11/18 – “Electric propulsion with power supplied within the vehicle”. As you might have expected there is a clear upward trend, and filings in this area exceeded those for internal combustion engines in 2017, and are rapidly moving away.

The New World seems to be winning this battle, but the Old World has not yet given up the fight. This is perhaps to be expected, electrified vehicles for many applications, heavy duty vehicles, long distance freight, etc, is not yet technically feasible, and likely won’t be for some time to come. Internal combustion engine development is therefore still needed to increase efficiency and reduce emissions, and with that development comes valuable intellectual property that the Giants are clearly looking to protect.

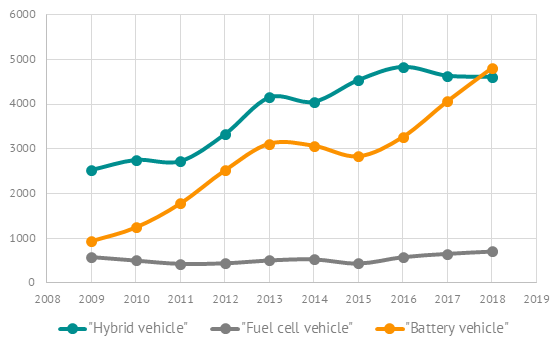

Before we look to see who is winning the battle of the New World, Figure 4. below shows us a simple breakdown of various technology solutions to electrify vehicles: Hybrid Electric Vehicles; Battery Electric Vehicles; and Fuel Cell Electric Vehicles. The most mature technology is clearly that of Hybrid Electric Vehicles, which have been on the market for many years in a bid to meet the ever more demanding emissions regulations. Despite the technology being mature, there has been a clear increase in the number of patent filings over the past 10 years, although the numbers of filings have now perhaps plateaued. No doubt the increase in filings is due to the term “Hybrid Electric Vehicle” encompassing technologies all the way from simple start-stop systems, through mild hybrid, full hybrid, and all the way to plug-in hybrid electric vehicles.

Where Hybrid Electric Vehicle patent filings have perhaps plateaued, Battery Electric Vehicles (BEVs) patent filings have increased, and appear to be continuing to increase rapidly. These two trends are clearly linked, the public desire for full BEVs is increasing, and manufacturers are responding with an ever increasing array of BEV models.

The same cannot be said for Fuel Cell Vehicles. Although the number of filings published in 2018 was 20% higher than 10 years previous, this pales into insignificance compared to the 400% or so increase in BEV filings. No doubt there are many reasons for the apparent lack of interest in Fuel Cell Vehicles, but the high cost of fuel cells, and the requirement for significant infrastructure investment to produce, distribute, store, and supply hydrogen (the dominant source of energy for fuel cells) clearly play a big role. As an interesting aside, nearly 30% of the patent filings over the past 10 years have been made by Toyota, adding further to the legend.

Figure 4.

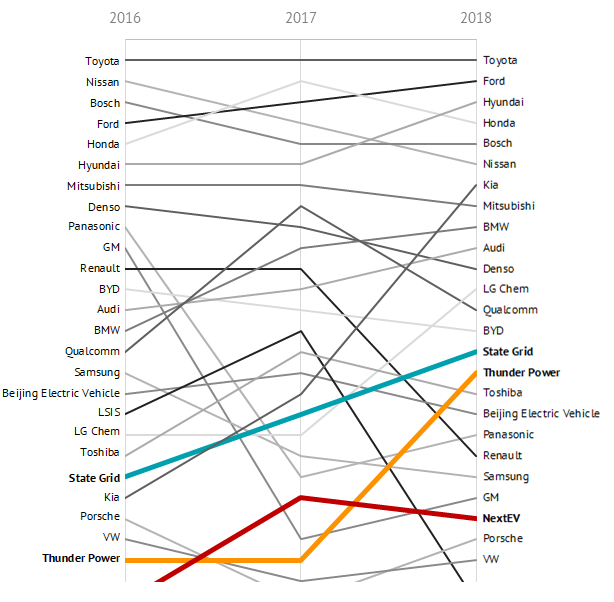

Given the significant increases in the number of patent filings in the New World of electrified powertrains, our searches looked into the companies that are filing in this area. Figure 5. below shows the evolution of the top 25 patent filers over the past three years in the IPC B60L 11/18 – “Electric propulsion with power supplied within the vehicle” – patent classification. The top 10 are perhaps not surprising, and comprise the Giants, including Toyota. However, I want to focus on the newcomers, the disruptors, whose technology and entrance into this market may cause concern for the incumbent OEMs.

I have highlighted three such newcomers, State Grid Corporation of China, Thunder Power Electric Vehicle, NextEV (now known as NIO, Inc.), who have been rising the list of top filers. All three are Chinese companies who have shown rapid growth in their relative patent filings over this period. State Grid, the Chinese state owned electricity utility, launched a charging network program in 2010, and are clearly looking to protect their IP in this area, as well as perhaps in technologies such as battery swapping to more closely match the “refill” time of gasoline.

Thunder Power Electric Vehicle and NextEV were both founded in 2014, and have since rapidly developed battery electric vehicles. Along with developing their vehicle models, they have clearly been protecting their IP, and not just in China. These Chinese “Minnows” are clearly innovators, and will likely present issues for the incumbent OEMs. The technological barriers to entry for BEVs are far lower than for more traditional internal combustion engine vehicles, and so given their clear desire to be innovators and only operate in the BEV market, the Giants of the Old World may see the Minnows of the New World winning battles, and perhaps even the war.

Figure 5.

Figure 5.

As another short aside, the “Minnow” NIO, Inc. (NextEV) currently has a market cap of around $6 Billion, not so small after all. In comparison, Ford Motor Company currently has a market cap of around $30 Billion, Renault around $18 Billion.

But perhaps there is some light at the end of the tunnel for the Giants. If we look at the patent classification H02P – “Control or Regulation of Electric Motors” – Figure 6., the applicant list is much more akin to what you would expect, some OEMs and some tier 1’s. Given all electric motors in electrified vehicles will require a control system of some form, it seems likely that some sort of more traditional supply arrangement, or perhaps some sort of cross-licensing will be needed.

Figure 6.

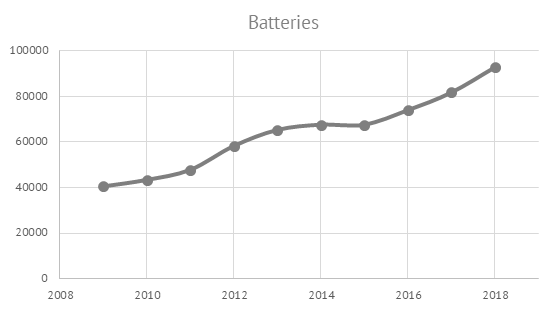

Before we bring this tale to an end, let us consider the other essential component of a BEV, the “B”. At present the cost of batteries is one of the brakes being applied to mainstream adoption by the market. Analysts predict that once batteries hit a price point around $100 per kWh, the cost brake at least will be released. There are many factors affecting the price of a battery, but technology is obviously one. Figure 7. below shows us that battery technology is in a phase of rapid development, with nearly 100,000 patent filings last year alone, compared to 40,000 10 years ago. This is a war still being fought, battery chemistry, manufacturing, and highly complex supply chains, being just a few of the battle fronts. Again, much like the powertrains themselves, it seems clear that collaboration will be needed here too, perhaps even standards essential patent pools.

Figure 7.

So how does our tale end? It seems clear that our first myth, that Internal Combustion Engines are a thing of the past, is just that, a myth not grounded in reality. The same appears true for our second myth, at least in the BEV market, Chinese companies are innovators.

However, the war between the Old World and the New is not yet over. Internal combustion engine development is clearly ongoing, and with good reason. Nevertheless, it seems that BEVs will win the war one day, but that day will not be in the near future. And what of the Giants and Minnows? Well, the incumbent OEMs are fighting hard, but the Minnows are too and will be difficult to beat. I suspect there will be casualties on both sides.

Originally presented at the Future Powertrains Conference 2019 at the National Motorcycle Museum, Coventry.

This article is for general information only. Its content is not a statement of the law on any subject and does not constitute advice. Please contact Reddie & Grose LLP for advice before taking any action in reliance on it.